Market Review:

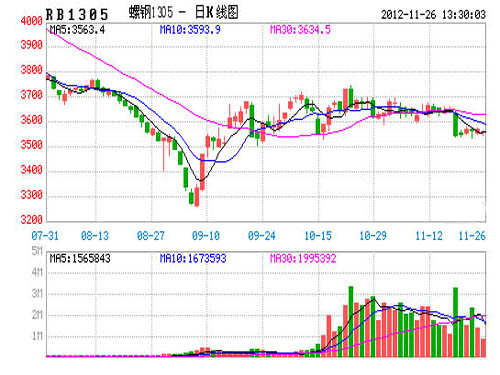

This week, the main thread contract RB1305 formed a small bullish candlestick pattern. The opening price this week was 3631, the highest was 3677, the lowest was 3620, and the closing price was 3643. This represents a 3% increase from the previous week, with a decrease of 0.08%. Trading volume was 7.981 million lots, and open interest was 1.003 million lots.

Factors impacting the market this week:

1. Steel spot market: Domestic steel markets continued to decline, with construction materials and profiles showing weakness. However, hot-rolled, medium plate, and cold-rolled products remained firm. Trade restrictions and out-of-stock situations became significant topics in the market, providing some support to prices. As weather conditions worsen and demand decreases, transaction volumes are expected to shrink further, making the market outlook less optimistic.

International factors:

BHP Billiton's CEO Wilson mentioned on Wednesday that the company plans to increase its iron ore production capacity by nearly one-fifth through enhanced operations in mines, railways, and ports. A sluggish iron ore market has prompted cost control measures, and uncertain demand in China has led many miners, including Brazil's Vale, to reconsider expansion plans. Global shipbuilding overcapacity, driven by declining orders, has particularly impacted Korea, the world's largest shipbuilder. Statistics show that from January to September, global new ship orders totaled only 14.34 million corrected gross tons, a 48% year-on-year decline. Despite receiving the largest number of orders at 5.2 million corrected tons (36%), South Korea still saw a 59% year-on-year drop. This downturn in the Korean shipbuilding industry has directly led to a decrease in plate production and demand. Data from the Korea Iron and Steel Association indicates that from January to September this year, Korean plate and ship plate production was 7.9 million tons, a 7% year-on-year decline. In September alone, production fell by 4% to 814,800 tons.

Domestic factors:

The National Development and Reform Commission announced a reduction in gasoline and diesel prices by RMB 310 and RMB 300 per ton, respectively, effective from midnight on November 16. This translates to a decrease of 0.23 yuan per liter for No. 90 gasoline and 0.26 yuan per liter for No. 0 diesel (national average). Additionally, the China Iron and Steel Industry Association stated that recent measures to stabilize growth have led to a slight rebound in the steel market since late September. It is anticipated that the steel market's demand situation will improve in the fourth quarter. Notably, the steel industry has faced continuous losses this year. Data from the China Iron and Steel Association shows that from January to September, the sales revenue of large and medium-sized steel companies decreased by 6.49% year-on-year, with losses reaching 26.726 billion yuan, 41.5 times higher than last year. Excess capacity remains a critical issue in the steel industry, leading to weak bargaining power domestically and upstream cost pressures, including iron ore prices, that cannot be fully passed on to downstream industries.

Construction steel:

Following a prolonged sideways market, construction steel prices fell this week. Dealers adjusted their prices, reflecting the influence of low-priced northern resources and a gradual enrichment of market resources, widening the cost gap. Downstream demand has weakened as winter approaches, with only some small-size and seismic resources remaining in demand. By Friday's close, the average price of HRB335 20mm rebar in 25 cities nationwide was RMB 3,821/ton, down RMB 31/ton from November 2. The national average price of HRB400 20mm threaded rebar was RMB 3,922/ton, down RMB 26/ton from November 9. The average price of Q235 6.5mm rebar in 24 major cities was RMB 3,766/ton, down RMB 32/ton from November 2. Differentiation in brand prices, especially in Shanghai, showed stable wire rod prices (3565, 0.00, 0.00%), falling spiral prices, and weakening threads. Thread manufacturers like Shente and Zhongtian frequently reduced prices this week, causing a decrease in three-brand thread resources. Overall, the current supply-demand dynamics remain strong. With resource replenishment underway, downward pressure on construction steel prices is inevitable, and a further decline is expected next week.

Latest production data from the China Steel Association shows that the daily crude steel production by key enterprises in late October was 1.5195 million tons, down 5.4% from the previous month. The national average daily crude steel production was 1.9277 million tons, down 3.7% from the previous month. These figures were more than market expectations, and when the data was released in mid-October, industry players generally expected daily crude steel production to rise above 1.95 million tons in October.

Production Costs:

(1) Iron Ore:

The domestic iron ore market remained stable overall this week, with minor regional declines. Some steel mills in the Tangshan area of Hebei Province were affected by the drop in billets, reducing their purchase prices by RMB 10-20/ton. Due to market resource tightness during the period of rumors, most merchants' quotations remained firm, but steel mills were dissatisfied.

The Hangxing area remained largely stable, with steel mills slowing purchases. Some merchants actively shipped goods, but low-priced transactions were poor. Currently, the ex-factory price of 66% Fe fine powder wet basis in Tangshan Zunhua is RMB 790-800/ton, down RMB 10/ton from last week. The 66% alkaline iron concentrate dry basis price in Hangxing Bureau is RMB 1005/ton (tax not included). Wu'an 64% alkaline iron powder wet basis (tax not included) is RMB 860-880/ton, down RMB 5/ton from last week. Shanxi Dai County 65% iron powder wet basis (tax not included) is RMB 760-770/ton.

The iron concentrate market in Liaoning remained stable this week, with rain and snow leading to a semi-stagnant market. Prices were firm but demand was sluggish, creating a pessimistic market sentiment. Current prices include: Jianping 66% iron concentrate wet basis ex-factory price at RMB 690-710/ton (within 10% moisture); Beipiao 66% iron concentrate wet basis ex-factory price at RMB 670-690/ton (within 12% moisture); the mainstream price of 65% iron powder concentrate in Anshan wet basis is RMB 690-700/ton; Liaoyang 65% iron powder base price is RMB 680-700/ton; Benxi 670-690 yuan/ton.

The iron ore fines market in East China remained stable this week, with tight market resources and good sales performance at mines. Recently, falling steel product prices have encouraged merchants to ship more actively. Current prices include: dry basis 64%-65% iron powder in Shandong Laiwu at RMB 1060/ton; 64% iron powder in Laizhou at around RMB 1030/ton; dry basis 64% iron powder in Maanshan, Anhui Province at RMB 930-950/ton; and 65% iron powder price in Fanchang, Tongling at RMB 980-1000/ton. The iron ore fines market price in Central and South China was stable this week, with increased purchases by steel mills and active market transactions. Current mainstream prices include: 64% iron powder dry basis in Guangdong Heyuan at RMB 850, and 65% iron powder dry basis in Huaiji at RMB 860; Hubei Daye 63% iron powder dry basis including tax at RMB 880/ton.

(2) Coke:

The domestic coke market maintained an overall upward trend this week, with the mainstream gaining RMB 50/ton. Some regions in Shandong and Hebei exceeded this range, while gains in Shanxi slowed down. On the 13th, Shenhua secondary metallurgical coke increased by RMB 50/ton, driving the secondary coke market in some regions of Northwest China and Hebei Province to rise; additionally, steel mills in Tangshan and Handan had positive enthusiasm for overall steel products, driving the coke market in Shanxi and Hebei to continue to increase, with individual high resources in the Tangshan area approaching RMB 1,700/ton. In the East China market, secondary metallurgical coke in Nippon Steel rose by RMB 100/ton in the middle of the week, driving up prices in markets such as Linyi and Rizhao in Shandong. The northeastern region experienced significantly reduced snowfall this week, with goods returning to normal. Some coking plants were reluctant to sell their goods, and prices were expected to rise. Coke in Henan’s Pingdingshan area rose by RMB 80, driven by high purchasing enthusiasm from steel buyers. In the short term, coke prices are expected to rise steadily. The coke market in southwest China traded well this week, with foreign coke prices rising by RMB 30, and short-term prices are prone to fluctuation. Mainstream reference prices in various regions are as follows: Shanxi Province's secondary metallurgical coke at RMB 1350-1380/ton, quasi-level metallurgical coke at RMB 1430-1480/ton (factory tax included), and metallurgical coke at RMB 1500-1550/ton (factory tax included); Hebei's coke market is steadily rising, with two-grade metallurgical coke at RMB 1480-1500/ton, Tangshan at RMB 1550-1620/ton (factory price); Xingtai quasi-first-grade metallurgical coke at RMB 1570-1590/ton (factory price), Tangshan at RMB 1660-1680/ton (factory price); Henan's coke market is stable, with two-grade metallurgical coke at RMB 1430-1480/ton, and first-grade metallurgical coke at RMB 1510-1530/ton (factory tax included); East China's coke market rose, with secondary metallurgical coke at RMB 1500-1550/ton, quasi-level at RMB 1550-1580/ton (factory tax included); Northeastern coke is temporarily stable, with two-grade metallurgical coke at RMB 1480-1520/ton, and quasi-level metallurgical coke at RMB 1610-1640/ton (factory tax included).

Port inventory: As of the 16th, my steel network's weekly port coke inventory statistics showed: Tianjin Port at 203.7 (down 10.3), Lianyungang at 20 (up 1), Rizhao Port at 8 (up 0.1) (in ten thousand tons); aspect: On the 16th, during the rally of 1305 futures, it broke through the 20-day moving average and closed at RMB 1588/ton, up 1.02%. Position decreased by 1890 lots, with 600,000 contracts traded.

(3) Ocean Shipping:

The maritime transportation market slowed this week. Continuing the slowdown in raw material import demand and the supply-demand contradiction caused by the delivery of new ships led to ongoing downward pressure on the market, bringing it closer to historical lows. As of the 6th, the BDI Index closed at 675 points, down 32 points or 4.52% from the same period last week. Capesize vessels rose unilaterally this week, with the BCI index closing at 1186 points, up 17 points or 1.45% from the same period last week. Domestic steel prices and ore prices have fallen sharply, prompting many steel mills to postpone the delivery date of long-term mines. Additionally, after previous Australian port overhauls caused delays in shipments, the arrival of ships in Hong Kong in the first half of the week supported the upward trend, but shipments slowed down in the second half of the week. Affected by domestic typhoon weather, ships at anchor gradually returned to the market to take possession of the goods, which could stop the market from rising and cause it to fall again. Statistics show that there are currently at least 350 sea-hull vessels in the market, representing about 25-30% of vessels with overcapacity. Currently, the average daily rent for Capesize vessels has been reported at $3466/day, up 6.64% this week. The Panamax ship was severely affected by heavy snow this week, with the BPI index closing at 617 points, down 141 points or 18.60% from the same period last week, the lowest since the end of January 2009. As the most new type of ships to be delivered, excess capacity has reached an unprecedented scale, and coal has not flourished during the peak season. The drought-stricken output of the South American grain market has been declining even further, and the freight rate hit a record low. This week, crushing occasional outflows in Indonesia and South America, but still unable to curb excess capacity, weighed on freight rates. Currently, Panamax boats have an average daily rent of $4,898/day, down 18.69% this week and down 62.11% from last year. The Supramax slowed down this week, with the BSI index closing at 837 points, down 18 points or 2.10% from the same period last week. The performance of the two oceans is the opposite. In the Atlantic region, only South America to Asia routes have been traded, freight rates have stabilized, and the rest of the lines have declined to varying degrees. The Pacific region benefited from the slight increase in coal import demand from India and Japan, and Indonesian exports gradually increased, with occasional mineral outflows in the region. Currently, the average daily rent of the Supramax boat is $8752/day, down 2.08% this week.

Downstream inventories:

Weak downstream demand continued this week, leading to some regional hoarding and a slight increase in the country's overall rebar inventory. At present, the country's major cities rebar inventory is 4,894,400 tons, compared to last week (November 9, 2012), this week's national rebar inventory increased by 0.60 million tons, an increase of 0.12%; compared to the same period last year (November 25, 2011), it decreased by 22,400 tons, a year-on-year decrease of 0.46%, with the decrease narrowing compared to the previous week.

Rebar stocks in most domestic cities this week still showed narrow changes. According to the ring comparison data, the changes in each region are as follows: East China decreased by 13,000 tons, Central China increased by 3.67 million tons, South China increased by 28,000 tons, Southwest China increased by 1.218 million tons, North China increased by 0.09 million tons, the Northwest decreased by 34,400 tons, and the Northeast decreased by 24,300 tons.

From the perspective of major cities, the cities with more obvious inventory changes this week are as follows: Wuhan's increase was 31,700 tons, Nanning's increase was 19,000 tons, Harbin's decrease was 22,000 tons, and Lanzhou's decrease was 20,000 tons; Shanghai's decrease was 11,100 tons.

This week, the total amount of domestic rebar stocks was reduced by 22,400 tons compared to the same period of last year, including a decrease of 92,500 tons in East China, an increase of 6,200 tons in Central China, a decrease of 17,000 tons in South China, an increase of 195,400 tons in Southwest China, a decrease in North China of 2.46 million tons, an increase of 25,400 tons in the Northwest region, and a decrease of 115,300 tons in the Northeast region.

With downstream demand continuing to decline and supply not declining significantly, most domestic cities have seen a decrease in rebar. As of the close of Friday, the average price of HRB335 material 20mm rebar from 25 cities nationwide was RMB 3818/ton, down RMB 30/ton from last week. The city with the largest drop was Changsha, which fell by RMB 130/t.

Market Outlook:

This week, downstream demand remained sluggish, with a more concentrated pessimistic atmosphere in the market. Prices of construction steel products generally showed a weak trend. In terms of inventory, inventories in the northwest and northeast regions continued to decline, while inventories in central, southern, southwestern, and northern China rose, and inventories in eastern China decreased. Looking at this week, along with the drop in temperature, local purchasing demand showed a weaker downward trend, and rebar prices in various markets gradually declined. Additionally, due to traffic control and weather conditions in parts of the area, the North Block was blocked, leading to significant resource overstocking in Jingtang Port and Bayuquan area. Consequently, the price drop in the northern region was particularly noticeable, further widening the north-south price gap. Under these circumstances, Hebei Iron & Steel issued the third-stage insurance policy within the year, requiring dealers not to sell below the limited price. This became a major factor in the market this week, slowing down the price drops in Beijing and Tianjin. Currently, the billet has gradually declined, weakening cost support. Together with the end of the *** and improving weather conditions, resources in the north will eventually move south. It is expected that rebar prices will continue to decline next week.

Market Review:

This week, the main thread contract RB1305 formed a small bullish candlestick pattern. The opening price this week was 3631, the highest was 3677, the lowest was 3620, and the closing price was 3643. This represents a 3% increase from the previous week, with a decrease of 0.08%. Trading volume was 7.981 million lots, and open interest was 1.003 million lots.

Factors impacting the market this week:

1. Steel spot market: Domestic steel markets continued to decline, with construction materials and profiles showing weakness. However, hot-rolled, medium plate, and cold-rolled products remained firm. Trade restrictions and out-of-stock situations became significant topics in the market, providing some support to prices. As weather conditions worsen and demand decreases, transaction volumes are expected to shrink further, making the market outlook less optimistic.

International factors:

BHP Billiton's CEO Wilson mentioned on Wednesday that the company plans to increase its iron ore production capacity by nearly one-fifth through enhanced operations in mines, railways, and ports. A sluggish iron ore market has prompted cost control measures, and uncertain demand in China has led many miners, including Brazil's Vale, to reconsider expansion plans. Global shipbuilding overcapacity, driven by declining orders, has particularly impacted Korea, the world's largest shipbuilder. Statistics show that from January to September, global new ship orders totaled only 14.34 million corrected gross tons, a 48% year-on-year decline. Despite receiving the largest number of orders at 5.2 million corrected tons (36%), South Korea still saw a 59% year-on-year drop. This downturn in the Korean shipbuilding industry has directly led to a decrease in plate production and demand. Data from the Korea Iron and Steel Association indicates that from January to September this year, Korean plate and ship plate production was 7.9 million tons, a 7% year-on-year decline. In September alone, production fell by 4% to 814,800 tons.

Domestic factors:

The National Development and Reform Commission announced a reduction in gasoline and diesel prices by RMB 310 and RMB 300 per ton, respectively, effective from midnight on November 16. This translates to a decrease of 0.23 yuan per liter for No. 90 gasoline and 0.26 yuan per liter for No. 0 diesel (national average). Additionally, the China Iron and Steel Industry Association stated that recent measures to stabilize growth have led to a slight rebound in the steel market since late September. It is anticipated that the steel market's demand situation will improve in the fourth quarter. Notably, the steel industry has faced continuous losses this year. Data from the China Iron and Steel Association shows that from January to September, the sales revenue of large and medium-sized steel companies decreased by 6.49% year-on-year, with losses reaching 26.726 billion yuan, 41.5 times higher than last year. Excess capacity remains a critical issue in the steel industry, leading to weak bargaining power domestically and upstream cost pressures, including iron ore prices, that cannot be fully passed on to downstream industries.

Construction steel:

Following a prolonged sideways market, construction steel prices fell this week. Dealers adjusted their prices, reflecting the influence of low-priced northern resources and a gradual enrichment of market resources, widening the cost gap. Downstream demand has weakened as winter approaches, with only some small-size and seismic resources remaining in demand. By Friday's close, the average price of HRB335 20mm rebar in 25 cities nationwide was RMB 3,821/ton, down RMB 31/ton from November 2. The national average price of HRB400 20mm threaded rebar was RMB 3,922/ton, down RMB 26/ton from November 9. The average price of Q235 6.5mm rebar in 24 major cities was RMB 3,766/ton, down RMB 32/ton from November 2. Differentiation in brand prices, especially in Shanghai, showed stable wire rod prices (3565, 0.00, 0.00%), falling spiral prices, and weakening threads. Thread manufacturers like Shente and Zhongtian frequently reduced prices this week, causing a decrease in three-brand thread resources. Overall, the current supply-demand dynamics remain strong. With resource replenishment underway, downward pressure on construction steel prices is inevitable, and a further decline is expected next week.

Latest production data from the China Steel Association shows that the daily crude steel production by key enterprises in late October was 1.5195 million tons, down 5.4% from the previous month. The national average daily crude steel production was 1.9277 million tons, down 3.7% from the previous month. These figures were more than market expectations, and when the data was released in mid-October, industry players generally expected daily crude steel production to rise above 1.95 million tons in October.

Production Costs:

(1) Iron Ore:

The domestic iron ore market remained stable overall this week, with minor regional declines. Some steel mills in the Tangshan area of Hebei Province were affected by the drop in billets, reducing their purchase prices by RMB 10-20/ton. Due to market resource tightness during the period of rumors, most merchants' quotations remained firm, but steel mills were dissatisfied.

The Hangxing area remained largely stable, with steel mills slowing purchases. Some merchants actively shipped goods, but low-priced transactions were poor. Currently, the ex-factory price of 66% Fe fine powder wet basis in Tangshan Zunhua is RMB 790-800/ton, down RMB 10/ton from last week. The 66% alkaline iron concentrate dry basis price in Hangxing Bureau is RMB 1005/ton (tax not included). Wu'an 64% alkaline iron powder wet basis (tax not included) is RMB 860-880/ton, down RMB 5/ton from last week. Shanxi Dai County 65% iron powder wet basis (tax not included) is RMB 760-770/ton.

The iron concentrate market in Liaoning remained stable this week, with rain and snow leading to a semi-stagnant market. Prices were firm but demand was sluggish, creating a pessimistic market sentiment. Current prices include: Jianping 66% iron concentrate wet basis ex-factory price at RMB 690-710/ton (within 10% moisture); Beipiao 66% iron concentrate wet basis ex-factory price at RMB 670-690/ton (within 12% moisture); the mainstream price of 65% iron powder concentrate in Anshan wet basis is RMB 690-700/ton; Liaoyang 65% iron powder base price is RMB 680-700/ton; Benxi 670-690 yuan/ton.

The iron ore fines market in East China remained stable this week, with tight market resources and good sales performance at mines. Recently, falling steel product prices have encouraged merchants to ship more actively. Current prices include: dry basis 64%-65% iron powder in Shandong Laiwu at RMB 1060/ton; 64% iron powder in Laizhou at around RMB 1030/ton; dry basis 64% iron powder in Maanshan, Anhui Province at RMB 930-950/ton; and 65% iron powder price in Fanchang, Tongling at RMB 980-1000/ton. The iron ore fines market price in Central and South China was stable this week, with increased purchases by steel mills and active market transactions. Current mainstream prices include: 64% iron powder dry basis in Guangdong Heyuan at RMB 850, and 65% iron powder dry basis in Huaiji at RMB 860; Hubei Daye 63% iron powder dry basis including tax at RMB 880/ton.

(2) Coke:

The domestic coke market maintained an overall upward trend this week, with the mainstream gaining RMB 50/ton. Some regions in Shandong and Hebei exceeded this range, while gains in Shanxi slowed down. On the 13th, Shenhua secondary metallurgical coke increased by RMB 50/ton, driving the secondary coke market in some regions of Northwest China and Hebei Province to rise; additionally, steel mills in Tangshan and Handan had positive enthusiasm for overall steel products, driving the coke market in Shanxi and Hebei to continue to increase, with individual high resources in the Tangshan area approaching RMB 1,700/ton. In the East China market, secondary metallurgical coke in Nippon Steel rose by RMB 100/ton in the middle of the week, driving up prices in markets such as Linyi and Rizhao in Shandong. The northeastern region experienced significantly reduced snowfall this week, with goods returning to normal. Some coking plants were reluctant to sell their goods, and prices were expected to rise. Coke in Henan’s Pingdingshan area rose by RMB 80, driven by high purchasing enthusiasm from steel buyers. In the short term, coke prices are expected to rise steadily. The coke market in southwest China traded well this week, with foreign coke prices rising by RMB 30, and short-term prices are prone to fluctuation. Mainstream reference prices in various regions are as follows: Shanxi Province's secondary metallurgical coke at RMB 1350-1380/ton, quasi-level metallurgical coke at RMB 1430-1480/ton (factory tax included), and metallurgical coke at RMB 1500-1550/ton (factory tax included); Hebei's coke market is steadily rising, with two-grade metallurgical coke at RMB 1480-1500/ton, Tangshan at RMB 1550-1620/ton (factory price); Xingtai quasi-first-grade metallurgical coke at RMB 1570-1590/ton (factory price), Tangshan at RMB 1660-1680/ton (factory price); Henan's coke market is stable, with two-grade metallurgical coke at RMB 1430-1480/ton, and first-grade metallurgical coke at RMB 1510-1530/ton (factory tax included); East China's coke market rose, with secondary metallurgical coke at RMB 1500-1550/ton, quasi-level at RMB 1550-1580/ton (factory tax included); Northeastern coke is temporarily stable, with two-grade metallurgical coke at RMB 1480-1520/ton, and quasi-level metallurgical coke at RMB 1610-1640/ton (factory tax included).

Port inventory: As of the 16th, my steel network's weekly port coke inventory statistics showed: Tianjin Port at 203.7 (down 10.3), Lianyungang at 20 (up 1), Rizhao Port at 8 (up 0.1) (in ten thousand tons); aspect: On the 16th, during the rally of 1305 futures, it broke through the 20-day moving average and closed at RMB 1588/ton, up 1.02%. Position decreased by 1890 lots, with 600,000 contracts traded.

(3) Ocean Shipping:

The maritime transportation market slowed this week. Continuing the slowdown in raw material import demand and the supply-demand contradiction caused by the delivery of new ships led to ongoing downward pressure on the market, bringing it closer to historical lows. As of the 6th, the BDI Index closed at 675 points, down 32 points or 4.52% from the same period last week. Capesize vessels rose unilaterally this week, with the BCI index closing at 1186 points, up 17 points or 1.45% from the same period last week. Domestic steel prices and ore prices have fallen sharply, prompting many steel mills to postpone the delivery date of long-term mines. Additionally, after previous Australian port overhauls caused delays in shipments, the arrival of ships in Hong Kong in the first half of the week supported the upward trend, but shipments slowed down in the second half of the week. Affected by domestic typhoon weather, ships at anchor gradually returned to the market to take possession of the goods, which could stop the market from rising and cause it to fall again. Statistics show that there are currently at least 350 sea-hull vessels in the market, representing about 25-30% of vessels with overcapacity. Currently, the average daily rent for Capesize vessels has been reported at $3466/day, up 6.64% this week. The Panamax ship was severely affected by heavy snow this week, with the BPI index closing at 617 points, down 141 points or 18.60% from the same period last week, the lowest since the end of January 2009. As the most new type of ships to be delivered, excess capacity has reached an unprecedented scale, and coal has not flourished during the peak season. The drought-stricken output of the South American grain market has been declining even further, and the freight rate hit a record low. This week, crushing occasional outflows in Indonesia and South America, but still unable to curb excess capacity, weighed on freight rates. Currently, Panamax boats have an average daily rent of $4,898/day, down 18.69% this week and down 62.11% from last year. The Supramax slowed down this week, with the BSI index closing at 837 points, down 18 points or 2.10% from the same period last week. The performance of the two oceans is the opposite. In the Atlantic region, only South America to Asia routes have been traded, freight rates have stabilized, and the rest of the lines have declined to varying degrees. The Pacific region benefited from the slight increase in coal import demand from India and Japan, and Indonesian exports gradually increased, with occasional mineral outflows in the region. Currently, the average daily rent of the Supramax boat is $8752/day, down 2.08% this week.

Downstream inventories:

Weak downstream demand continued this week, leading to some regional hoarding and a slight increase in the country's overall rebar inventory. At present, the country's major cities rebar inventory is 4,894,400 tons, compared to last week (November 9, 2012), this week's national rebar inventory increased by 0.60 million tons, an increase of 0.12%; compared to the same period last year (November 25, 2011), it decreased by 22,400 tons, a year-on-year decrease of 0.46%, with the decrease narrowing compared to the previous week.

Rebar stocks in most domestic cities this week still showed narrow changes. According to the ring comparison data, the changes in each region are as follows: East China decreased by 13,000 tons, Central China increased by 3.67 million tons, South China increased by 28,000 tons, Southwest China increased by 1.218 million tons, North China increased by 0.09 million tons, the Northwest decreased by 34,400 tons, and the Northeast decreased by 24,300 tons.

From the perspective of major cities, the cities with more obvious inventory changes this week are as follows: Wuhan's increase was 31,700 tons, Nanning's increase was 19,000 tons, Harbin's decrease was 22,000 tons, and Lanzhou's decrease was 20,000 tons; Shanghai's decrease was 11,100 tons.

This week, the total amount of domestic rebar stocks was reduced by 22,400 tons compared to the same period of last year, including a decrease of 92,500 tons in East China, an increase of 6,200 tons in Central China, a decrease of 17,000 tons in South China, an increase of 195,400 tons in Southwest China, a decrease in North China of 2.46 million tons, an increase of 25,400 tons in the Northwest region, and a decrease of 115,300 tons in the Northeast region.

With downstream demand continuing to decline and supply not declining significantly, most domestic cities have seen a decrease in rebar. As of the close of Friday, the average price of HRB335 material 20mm rebar from 25 cities nationwide was RMB 3818/ton, down RMB 30/ton from last week. The city with the largest drop was Changsha, which fell by RMB 130/t.

Market Outlook:

This week, downstream demand remained sluggish, with a more concentrated pessimistic atmosphere in the market. Prices of construction steel products generally showed a weak trend. In terms of inventory, inventories in the northwest and northeast regions continued to decline, while inventories in central, southern, southwestern, and northern China rose, and inventories in eastern China decreased. Looking at this week, along with the drop in temperature, local purchasing demand showed a weaker downward trend, and rebar prices in various markets gradually declined. Additionally, due to traffic control and weather conditions in parts of the area, the North Block was blocked, leading to significant resource overstocking in Jingtang Port and Bayuquan area. Consequently, the price drop in the northern region was particularly noticeable, further widening the north-south price gap. Under these circumstances, Hebei Iron & Steel issued the third-stage insurance policy within the year, requiring dealers not to sell below the limited price. This became a major factor in the market this week, slowing down the price drops in Beijing and Tianjin. Currently, the billet has gradually declined, weakening cost support. Together with the end of the *** and improving weather conditions, resources in the north will eventually move south. It is expected that rebar prices will continue to decline next week.

Biochemical Incubator is suitable for scientific research institutions, colleges and universities, production units or department laboratories of environmental protection, health and epidemic prevention, drug inspection, agriculture, livestock, aquatic products and other industries as important test equipment. It is a special constant temperature equipment for water analysis and BOD determination, cultivation, preservation, plant cultivation and breeding test of bacteria, mold and microorganism

Mould incubator,Intelligent biochemical incubator,Biochemical incubator

Zenith Lab (Jiangsu) Co.,Ltd , https://www.zenithlabo.com