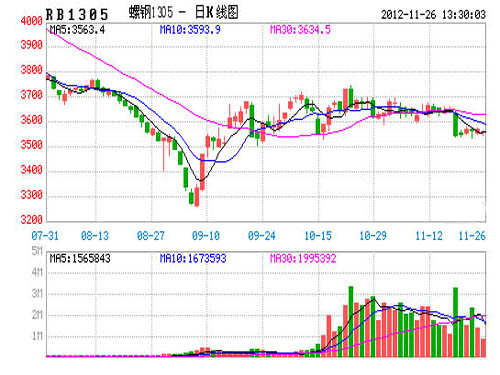

Market Review:

The K-line chart shows that the main contract RB1305 closed with a small bullish candlestick. This week's opening price was 3631, the highest price was 3677, the lowest price was 3620, and the closing price was 3643, representing a 3% increase from the previous week with a decrease of 0.08%. The trading volume was 7.981 million lots, and the open interest was 1.003 million lots.

Factors Impacting the Market:

1. Steel Spot Market: The domestic steel market continued to fall this week. Building materials and profiles saw weak downward trends, while hot-rolled, medium plates, and cold-rolled products remained firm. However, the market has seen a certain degree of "stannio," and stockouts have become a major talking point, which has been a significant factor in supporting prices. As the weather increasingly affects demand, trading volumes will likely decrease further, making the market outlook less optimistic. Details include:

- International: BHP Billiton's CEO stated that the company plans to increase its iron ore production capacity by nearly one-fifth by enhancing operations in mines, railways, and ports. The sluggish iron ore market has allowed the company to consider cost control measures. The weak demand in China has made the iron ore price outlook unclear, prompting most iron ore miners, including Vale, to reconsider expansion plans.

- Domestic: The National Development and Reform Commission announced a reduction in gasoline and diesel prices by RMB 310 and RMB 300 per ton respectively from November 16th. This has led to a decrease in the national average price of No. 90 gasoline and No. 0 diesel by 0.23 and 0.26 yuan per liter respectively. The China Iron and Steel Industry Association reported that the country has intensified measures to stabilize growth, leading to a slight rebound in steel prices since late September. It is anticipated that the steel market will see improved demand in the fourth quarter.

Construction Steel: After a prolonged sideways market, building materials prices fell this week. Merchant prices shifted from darker to brighter tones. On one hand, low-priced northern resources have enriched market resources, widening the cost gap. On the other hand, downstream demand has weakened with the approach of winter. Currently, except for small-size and seismic resources, mainstream resources face difficulty in shipping. By Friday's close, the average price of HRB335 20mm rebar across 25 cities nationwide was RMB 3,821/ton, a slight decrease of RMB 31/ton from November 2nd. The national average price of HRB400 20mm threaded rebar was RMB 3,922/ton, down 26 yuan/ton from November 9th. The national average price of Q235 6.5mm specification rebar was 3,766 yuan/ton, down 32 yuan/ton from November 2nd. Additionally, brand price differentiation, particularly in Shanghai, showed stable wire rod prices (3565, 0.00, 0.00%), falling spirals, and weakening threads. Among these, thread manufacturers like Shente and Zhongtian have seen frequent price cuts by agents this week, reducing the three-brand thread resources from the previous period. Overall, the current supply-demand pattern remains strong. With resource replenishment gradually occurring, downward pressure on construction steel prices is inevitable, and it is expected that prices will fall further next week.

Latest Data: The daily production of crude steel by key enterprises in late October was 1.5195 million tons, down 5.4% from the previous month; the national average production of crude steel was 1,927,700 tons, down 3.7% from the previous month. These figures were significantly higher than market expectations, surprising industry players who initially believed that daily crude steel production would rise to over 195 million tons in October.

Production Costs:

- Iron Ore: The domestic market for ore fines remained stable overall, with minor declines in specific regions. Some steel mills in the Tangshan area of Hebei Province were affected by the drop in billets, lowering their purchase price by RMB 10-20/t. Due to tight market resources during the period of rumors, most merchant quotes remained firm, though steel mills were generally dissatisfied.

- Coke: The domestic coke market maintained an overall upward trend, with the mainstream gaining RMB 50/ton, and individual regions in Shandong and Hebei above this range, while the Shanxi region's gains slowed down. On the 13th, Shenhua raised its secondary metallurgical coke by RMB 50/ton, driving the secondary coke market in some regions of Northwest China and Hebei Province to rise; additionally, steel mills in Tangshan and Handan had positive enthusiasm for overall steel products, driving the coke market in Shanxi and Hebei to continue increasing. In Tangshan, individual high resources were close to RMB 1,700/ton.

Market Outlook:

This week, downstream demand remained sluggish, causing resources in some regions to be hoarded, which led to a slight increase in the country's overall rebar inventory. Currently, the country's major cities rebar inventory is 4,894,400 tons, compared with last week (November 9th), this week's national rebar inventory rose by 0.60 million tons, an increase of 0.12%; compared with the same period last year (November 25th), it decreased by 22,400 tons, a year-on-year decrease of 0.46%, with the decrease narrowing compared to the previous week.

Rebar stocks in most domestic cities this week still showed a narrow range of changes. According to the ring comparison data, the changes in each region were as follows: a 13,000-ton reduction in East China, a 3.67-million-ton increase in Central China, a 28,000-ton increase in South China, a 1.218-million-ton increase in Southwest China, and a 0.09-million-ton increase in North China. The northwest region saw a 34,400-ton reduction, and the northeast region saw a 24,300-ton reduction.

From the perspective of major cities, the cities with more obvious inventory changes this week were as follows: Wuhan's increase was 31,700 tons, Nanning's increase was 19,000 tons, Harbin's reduction was 22,000 tons, and Lanzhou's reduction was 20,000 tons; Shanghai's reduction was 11,100 tons.

This week, the total domestic rebar stocks were reduced by 22,400 tons compared to the same period last year, including a 92,500-ton reduction in East China, a 6,200-ton increase in Central China, a 17,000-ton reduction in South China, a 195,400-ton increase in Southwest China, a 2.46-million-ton reduction in North China, a 25,400-ton increase in Northwest China, and a 115,300-ton reduction in Northeast China.

With downstream demand continuing to decline and supply not declining significantly, most domestic cities have seen a decline in rebar. As of Friday's close, the average price of HRB335 20mm rebar from 25 cities nationwide was RMB 3818/ton, which was RMB 30/ton lower than last week. The city with the largest drop was Changsha, with a decrease of RMB 130/t.

Market Outlook:

This week, downstream demand continued to be sluggish. The pessimistic atmosphere in the market became more concentrated. The prices of construction steel products generally showed a weak trend. In terms of inventory, inventories in the northwest and northeast regions continued to decline, while inventories in central, southern, southwestern, and northern China rose, and inventories in eastern China decreased. Looking at this week, along with the drop in temperature, local purchasing demand showed a weaker downward trend, and the prices of rebars in various markets gradually declined. Additionally, due to traffic control and weather conditions in some areas, the Northern Block was blocked, and resources in Jingtang Port and Bayuquan area were significantly overstretched. Therefore, the price drop was particularly noticeable in the northern region, and the difference between north and south widened further. Under these circumstances, Hebei Iron & Steel issued the third-stage insurance policy within the year, requiring dealers not to sell below the limited price. This has become a major aspect of the market this week, and thus the price declines in Beijing and Tianjin slowed down. At present, the billet has gradually declined, and the cost support has weakened. Together with the end of the *** and the improved weather, resources in the north will eventually go south. It is expected that the price of rebar will continue to decline next week.

Market Review:

The K-line chart shows that the main contract RB1305 closed with a small bullish candlestick. This week's opening price was 3631, the highest price was 3677, the lowest price was 3620, and the closing price was 3643, representing a 3% increase from the previous week with a decrease of 0.08%. The trading volume was 7.981 million lots, and the open interest was 1.003 million lots.

Factors Impacting the Market:

1. Steel Spot Market: The domestic steel market continued to fall this week. Building materials and profiles saw weak downward trends, while hot-rolled, medium plates, and cold-rolled products remained firm. However, the market has seen a certain degree of "stannio," and stockouts have become a major talking point, which has been a significant factor in supporting prices. As the weather increasingly affects demand, trading volumes will likely decrease further, making the market outlook less optimistic. Details include:

- International: BHP Billiton's CEO stated that the company plans to increase its iron ore production capacity by nearly one-fifth by enhancing operations in mines, railways, and ports. The sluggish iron ore market has allowed the company to consider cost control measures. The weak demand in China has made the iron ore price outlook unclear, prompting most iron ore miners, including Vale, to reconsider expansion plans.

- Domestic: The National Development and Reform Commission announced a reduction in gasoline and diesel prices by RMB 310 and RMB 300 per ton respectively from November 16th. This has led to a decrease in the national average price of No. 90 gasoline and No. 0 diesel by 0.23 and 0.26 yuan per liter respectively. The China Iron and Steel Industry Association reported that the country has intensified measures to stabilize growth, leading to a slight rebound in steel prices since late September. It is anticipated that the steel market will see improved demand in the fourth quarter.

Construction Steel: After a prolonged sideways market, building materials prices fell this week. Merchant prices shifted from darker to brighter tones. On one hand, low-priced northern resources have enriched market resources, widening the cost gap. On the other hand, downstream demand has weakened with the approach of winter. Currently, except for small-size and seismic resources, mainstream resources face difficulty in shipping. By Friday's close, the average price of HRB335 20mm rebar across 25 cities nationwide was RMB 3,821/ton, a slight decrease of RMB 31/ton from November 2nd. The national average price of HRB400 20mm threaded rebar was RMB 3,922/ton, down 26 yuan/ton from November 9th. The national average price of Q235 6.5mm specification rebar was 3,766 yuan/ton, down 32 yuan/ton from November 2nd. Additionally, brand price differentiation, particularly in Shanghai, showed stable wire rod prices (3565, 0.00, 0.00%), falling spirals, and weakening threads. Among these, thread manufacturers like Shente and Zhongtian have seen frequent price cuts by agents this week, reducing the three-brand thread resources from the previous period. Overall, the current supply-demand pattern remains strong. With resource replenishment gradually occurring, downward pressure on construction steel prices is inevitable, and it is expected that prices will fall further next week.

Latest Data: The daily production of crude steel by key enterprises in late October was 1.5195 million tons, down 5.4% from the previous month; the national average production of crude steel was 1,927,700 tons, down 3.7% from the previous month. These figures were significantly higher than market expectations, surprising industry players who initially believed that daily crude steel production would rise to over 195 million tons in October.

Production Costs:

- Iron Ore: The domestic market for ore fines remained stable overall, with minor declines in specific regions. Some steel mills in the Tangshan area of Hebei Province were affected by the drop in billets, lowering their purchase price by RMB 10-20/t. Due to tight market resources during the period of rumors, most merchant quotes remained firm, though steel mills were generally dissatisfied.

- Coke: The domestic coke market maintained an overall upward trend, with the mainstream gaining RMB 50/ton, and individual regions in Shandong and Hebei above this range, while the Shanxi region's gains slowed down. On the 13th, Shenhua raised its secondary metallurgical coke by RMB 50/ton, driving the secondary coke market in some regions of Northwest China and Hebei Province to rise; additionally, steel mills in Tangshan and Handan had positive enthusiasm for overall steel products, driving the coke market in Shanxi and Hebei to continue increasing. In Tangshan, individual high resources were close to RMB 1,700/ton.

Market Outlook:

This week, downstream demand remained sluggish, causing resources in some regions to be hoarded, which led to a slight increase in the country's overall rebar inventory. Currently, the country's major cities rebar inventory is 4,894,400 tons, compared with last week (November 9th), this week's national rebar inventory rose by 0.60 million tons, an increase of 0.12%; compared with the same period last year (November 25th), it decreased by 22,400 tons, a year-on-year decrease of 0.46%, with the decrease narrowing compared to the previous week.

Rebar stocks in most domestic cities this week still showed a narrow range of changes. According to the ring comparison data, the changes in each region were as follows: a 13,000-ton reduction in East China, a 3.67-million-ton increase in Central China, a 28,000-ton increase in South China, a 1.218-million-ton increase in Southwest China, and a 0.09-million-ton increase in North China. The northwest region saw a 34,400-ton reduction, and the northeast region saw a 24,300-ton reduction.

From the perspective of major cities, the cities with more obvious inventory changes this week were as follows: Wuhan's increase was 31,700 tons, Nanning's increase was 19,000 tons, Harbin's reduction was 22,000 tons, and Lanzhou's reduction was 20,000 tons; Shanghai's reduction was 11,100 tons.

This week, the total domestic rebar stocks were reduced by 22,400 tons compared to the same period last year, including a 92,500-ton reduction in East China, a 6,200-ton increase in Central China, a 17,000-ton reduction in South China, a 195,400-ton increase in Southwest China, a 2.46-million-ton reduction in North China, a 25,400-ton increase in Northwest China, and a 115,300-ton reduction in Northeast China.

With downstream demand continuing to decline and supply not declining significantly, most domestic cities have seen a decline in rebar. As of Friday's close, the average price of HRB335 20mm rebar from 25 cities nationwide was RMB 3818/ton, which was RMB 30/ton lower than last week. The city with the largest drop was Changsha, with a decrease of RMB 130/t.

Market Outlook:

This week, downstream demand continued to be sluggish. The pessimistic atmosphere in the market became more concentrated. The prices of construction steel products generally showed a weak trend. In terms of inventory, inventories in the northwest and northeast regions continued to decline, while inventories in central, southern, southwestern, and northern China rose, and inventories in eastern China decreased. Looking at this week, along with the drop in temperature, local purchasing demand showed a weaker downward trend, and the prices of rebars in various markets gradually declined. Additionally, due to traffic control and weather conditions in some areas, the Northern Block was blocked, and resources in Jingtang Port and Bayuquan area were significantly overstretched. Therefore, the price drop was particularly noticeable in the northern region, and the difference between north and south widened further. Under these circumstances, Hebei Iron & Steel issued the third-stage insurance policy within the year, requiring dealers not to sell below the limited price. This has become a major aspect of the market this week, and thus the price declines in Beijing and Tianjin slowed down. At present, the billet has gradually declined, and the cost support has weakened. Together with the end of the *** and the improved weather, resources in the north will eventually go south. It is expected that the price of rebar will continue to decline next week.

Refrigerated Centrifuge is divided into low speed, high speed refrigerated centrifuge, as well as overspeed analysis, preparation of dual-use refrigerated centrifuge and other models.

Refrigerated Centrifuge,High speed refrigerated centrifuge,Low speed refrigerated centrifuge

Zenith Lab (Jiangsu) Co.,Ltd , https://www.zenithlabo.com